Academic Libraries: Where Reference Goes to Die.

Facing the Most Profound Structural Transformation of Any Library Sector - four of multi-part review of the US library market

At the end of 2017, ARL research libraries crossed an historic line: collections spending surpassed personnel as the largest budget category. For the first time, the cost of accessing information exceeds the cost of the people who make that access possible. Since this economic balance changed, everything downstream has also shifted — staffing levels, the viability of legacy service models, and even the definition of what it means to “use” scholarly content in an environment where systems have removed inconvenience and inefficiency.

The changing economics of information are reshaping everything downstream: how many staff get hired, whether inter-library loan makes operational sense, what “reading a journal article” even means in a world where AI systems present peer-reviewed literature in real time. This is a sector in a more profound transformation than any other in the library landscape, and the data across every dimension of the ARL and NCES surveys makes that undeniable.

Key Data — Academic Libraries

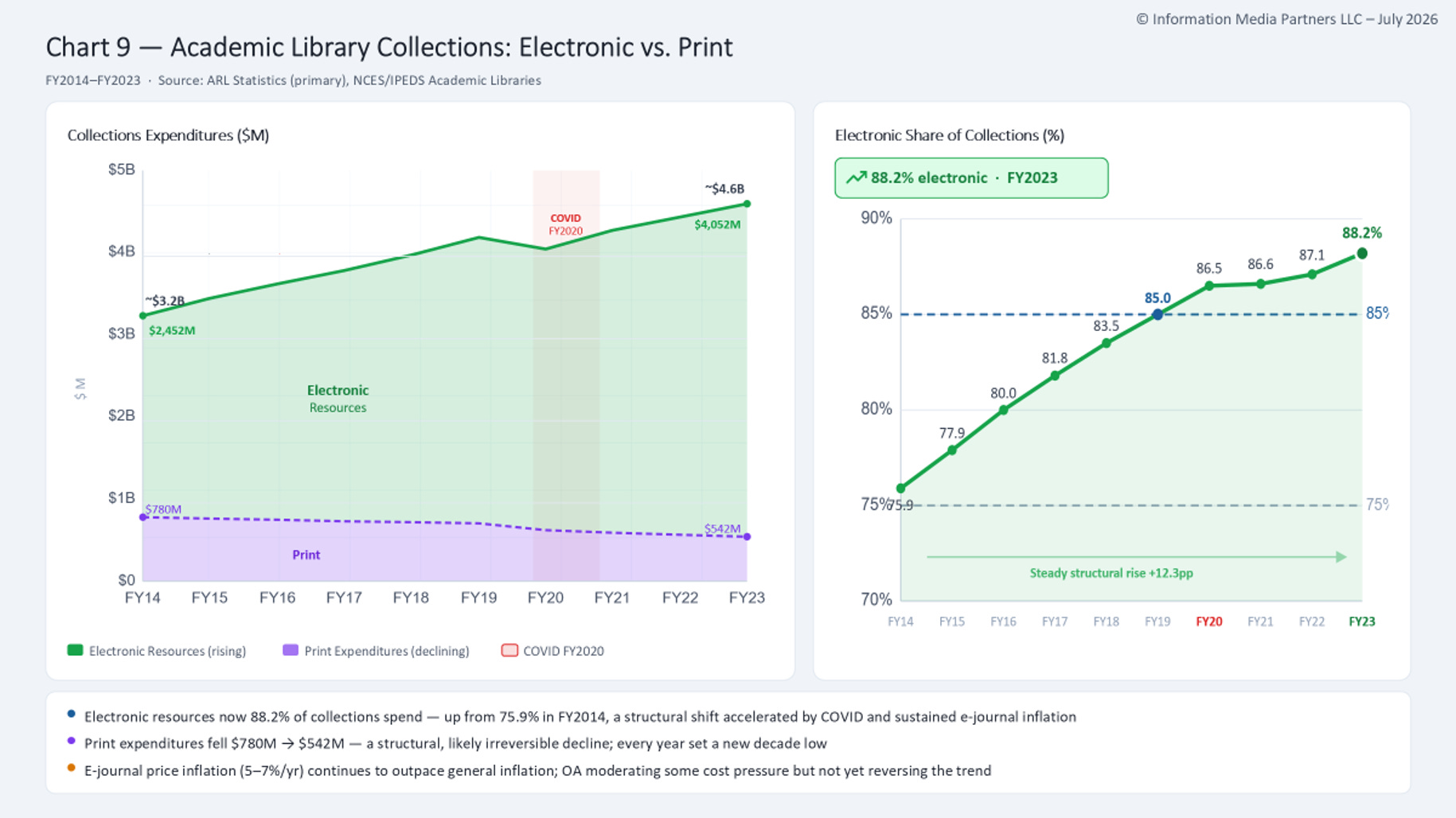

88.2% — Electronic share of collections expenditures at ARL libraries in FY2023 (up from 75.9% in FY2014)

+273% — Growth in open access journal titles (DOAJ), FY2014–FY2023 (9,800 → 36,500)

−17% — Decline in academic ILL borrowed items, FY2014–FY2019 (pre‑COVID), driven by open access

From a presentation in 2010, I dug into the changing mix of books and electronic resources.

Lonesome: ILL in Structural Decline

Publishers have never been completely comfortable with inter-libary loan so will be sanguine that Academic ILL borrowed items fell from 7.82 million in FY2014 to 6.48 million in FY2019 — a 17% drop with no pandemic. This decline in the absence of service disruption, and no operational shock. COVID pushed the number down further, but even after a full recovery of infrastructure, ILL is still well below the FY2014 baseline.

Driving this change is open access. When roughly one‑third of peer‑reviewed literature is freely available through OA journals, institutional repositories, and preprint servers, researchers will bypass ILL (and the librarian) entirely. Scholars get the article immediately, at no cost, without waiting 3–10 business days or triggering a $12–$25 transaction. Patron behavior is rational, and the shift is structural and workflow improvements won’t reverse it. If anything, libraries will encourage further workflow improvements.

Open Access Comes Faster and Faster

The scale of the OA transition is one of the defining developments in scholarly communication:

OA journal titles (DOAJ): 9,800 → 36,500 (+273%)

Institutional Repository (IR) deposits (cumulative): 18M → 98M (+444%)

Annual OA downloads: 285M → 2.05B (+620%)

OA share of peer‑reviewed literature: ~15% → ~35%

The 2022 OSTP memorandum — requiring immediate public access to federally funded research by 2025 — is the most consequential federal action in this space in decades (ever?). IR growth will accelerate sharply as agencies accelerate compliance. Libraries are the functional backbone for that compliance, and this is one area where their operational footprint is expanding.

Collections vs. Staff: A Sustainability Crisis

ARL operating budgets grew from $7.09B (FY2014) to $8.98B (FY2023). Inside that growth, the internal balance shifted dramatically:

Staff costs: $3.18B → $3.61B (+14%), falling from 45% to 40% of total

Collections: $3.23B → $4.59B (+42%), rising from 46% to 51% of total

Electronic resources are now dominant:

Electronic spend: $2.45B → $4.05B (+65%), now 88.2% of collections

Print spend: $780M → $542M (−30.5%)

The driver is subscription inflation of 5–7% annually — well above CPI and well above library budget growth. As collections consume more of the budget, staffing contracts. The five‑point drop in staff share represents real positions not filled and left vacant and subject expertise lost. This collections‑versus‑staff squeeze is the central sustainability problem for academic libraries over the next decade. (Incidentally, MLIS degreed candidates can look forward to good job prospects according to this research).

Enrollment Declines Distort Per‑Student Metrics

Analysts have been predicting that student enrollment will ‘fall off a cliff’ right about now and these 10 year numbers confirm this trend. U.S. higher education enrollment fell from 20.2M (FY2014) to 17.6M (FY2023), a 13% decline. When the denominator shrinks, per‑student metrics inflate artificially:

Collections spend per student: $182 → $240 (+32%)

Library visits per student: 8.2 → 4.8 (FY2023), only 59% of the FY2014 baseline

Reference transactions per student: 1.85 → 1.18

When will libraries refuse to pay the FTE based subscriptions and refactor their base subscription fees? With researchers more self‑sufficient and efficient, overall declining student populations, reduction of academic programs, and user stats showing declining engagement metrics libraries will require stronger evidence of value. There is no question academic libraries need these resources to maintain enrollment and attract new students but is that at any price?

The 2025–2027 Outlook

Academic libraries face the most difficult environment of any sector in this analysis:

Electronic share will likely exceed 90% by FY2026

OA mandates will accelerate IR growth. Institutions will dictate more IR policy

Enrollment declines — especially at regional institutions — will trigger budget cuts that hit staffing first. Some predict a 20% closure rate.

AI‑driven changes to usage metrics will complicate Big Deal negotiations and weaken traditional evidence of value unless new measures are adopted and accepted

The academic library’s value is real and well‑documented. The challenge is that the metrics used to demonstrate that value are eroding just as the sector enters its most consequential period of change.

Librarians, provosts and other relevant administrators are not ignorant of the (good) financial performance of many of the largest library vendors and publishers. Thusfar, attempts to reduce the ‘big deal’ and the customary annual increases across the board have engendered modest push back. (Probably the most notable was the UC system). But we will see significant changes in collections management, pricing, renewals and publishing deals in the next five years because there are are many more factors at play now versus 10 years ago: OA, enrollment, market size reduction, and stronger adoption of research copyrights will all play significant roles in a realignment across the academic community.

Look for the next post in this series on the HR problems facing libraries. See the earlier posts for the intro to the series.

Full Library Presentation 2014 - 2023

Michael Cairns is a senior publishing executive and consultant. He can be reached at michael. cairns @ outlook.com or 908 938 4889